The Short Call

Get Paid to Sell Shares or Short a Stock

This week we are going to discuss The Short Call. By itself, it’s not one I do often. But many do these as a Covered Call, which we will get into below!

Details

The Short Call can be done Naked (without 100 shares owned) or Covered (with 100 shares owned). One does need Level 4 Options in order to trade Short Calls Naked. Level 2 is required for Covered Calls. If Naked, all we are doing is selling a Call at a strike we believe the stock will not breach by expiration. If Covered, a trader is picking a strike at a price they would be happy to sell their shares at. The strike could be Out the Money (OTM), At the Money (ATM) or In the Money (ITM). It’s all depending on the trader’s risk tolerance and how aggressive they want to be with their assumption.

One thing to mention, NEVER sell Covered Calls on shares you DON’T want to sell. You may ignore this piece of advice, that’s okay. However, you will learn why I recommend this. It is something I learned through experience.

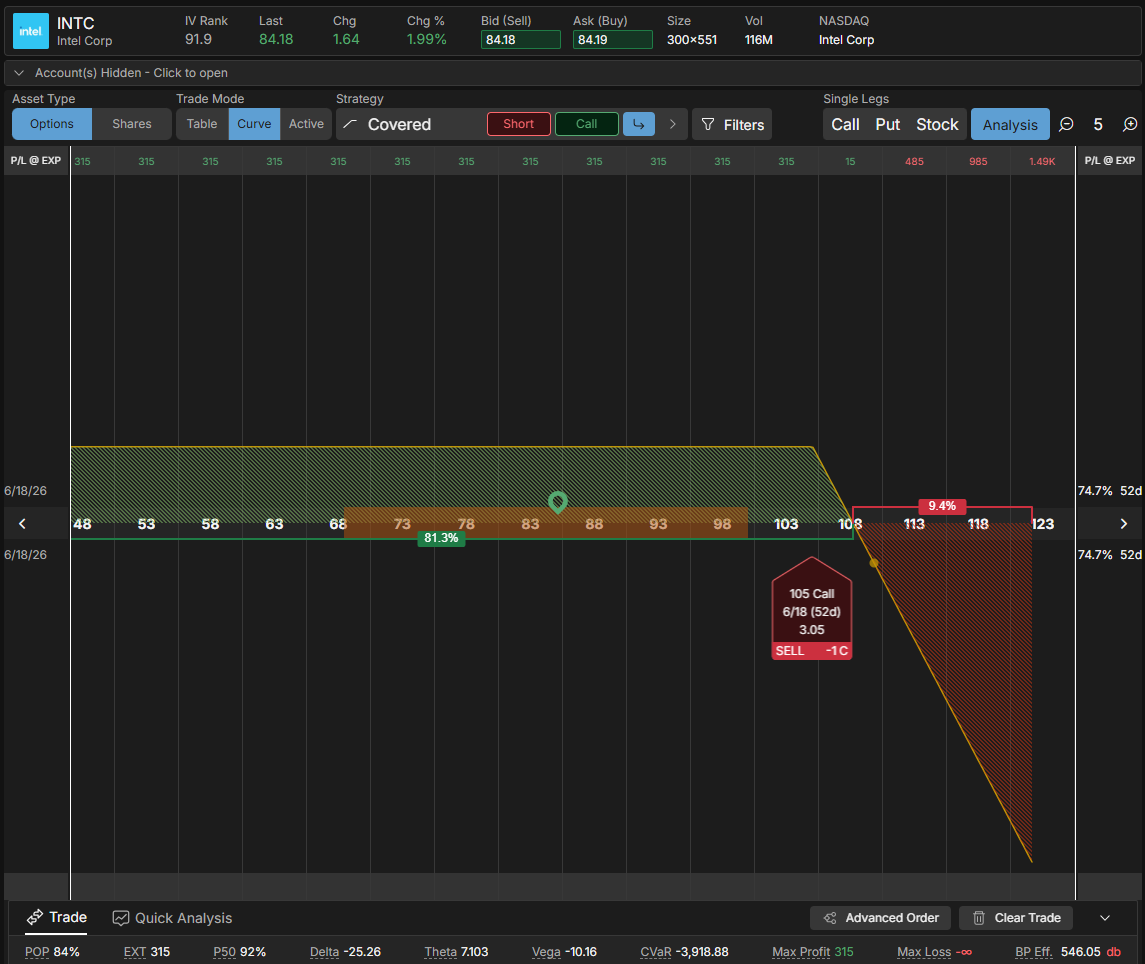

Traditionally, a Short Call is selling an OTM or ATM strike. However, one could place the Short strike at whatever price they want. I usually structure this trade with my strike OTM. I aim for somewhere around the 15 to 30Δ (usually landing around the 20-ishΔ). I also use the expected move to assist which strike I select. For the purposes of this post, I am going to focus on structuring this with the strike OTM. Below is an example Naked Short Call profit and loss graph in Intel (INTC).

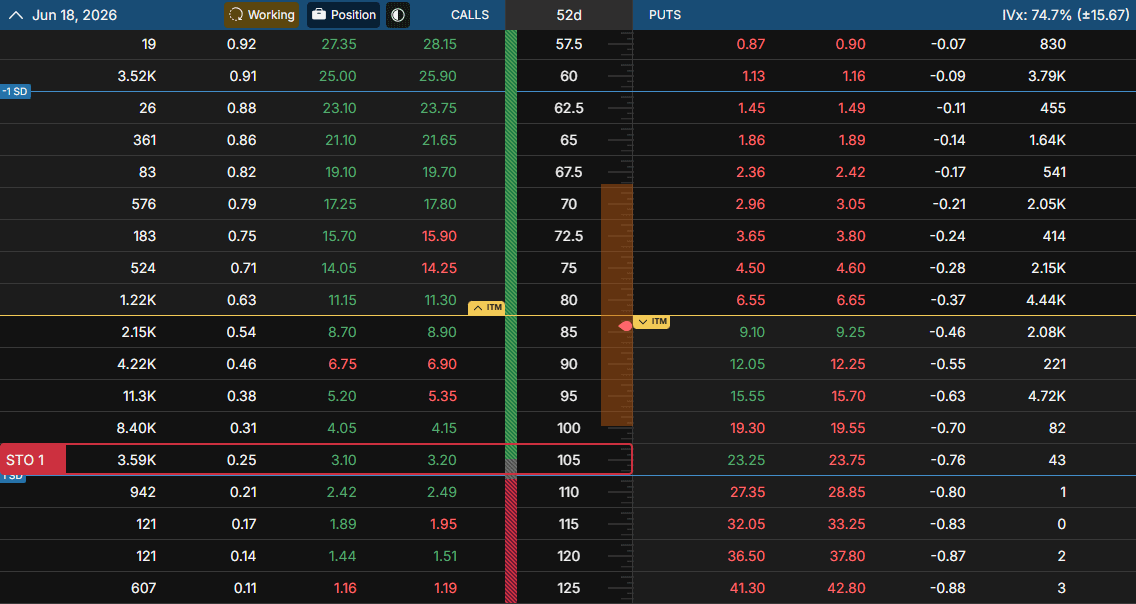

The image below shows how this trade would be structured in an options table.

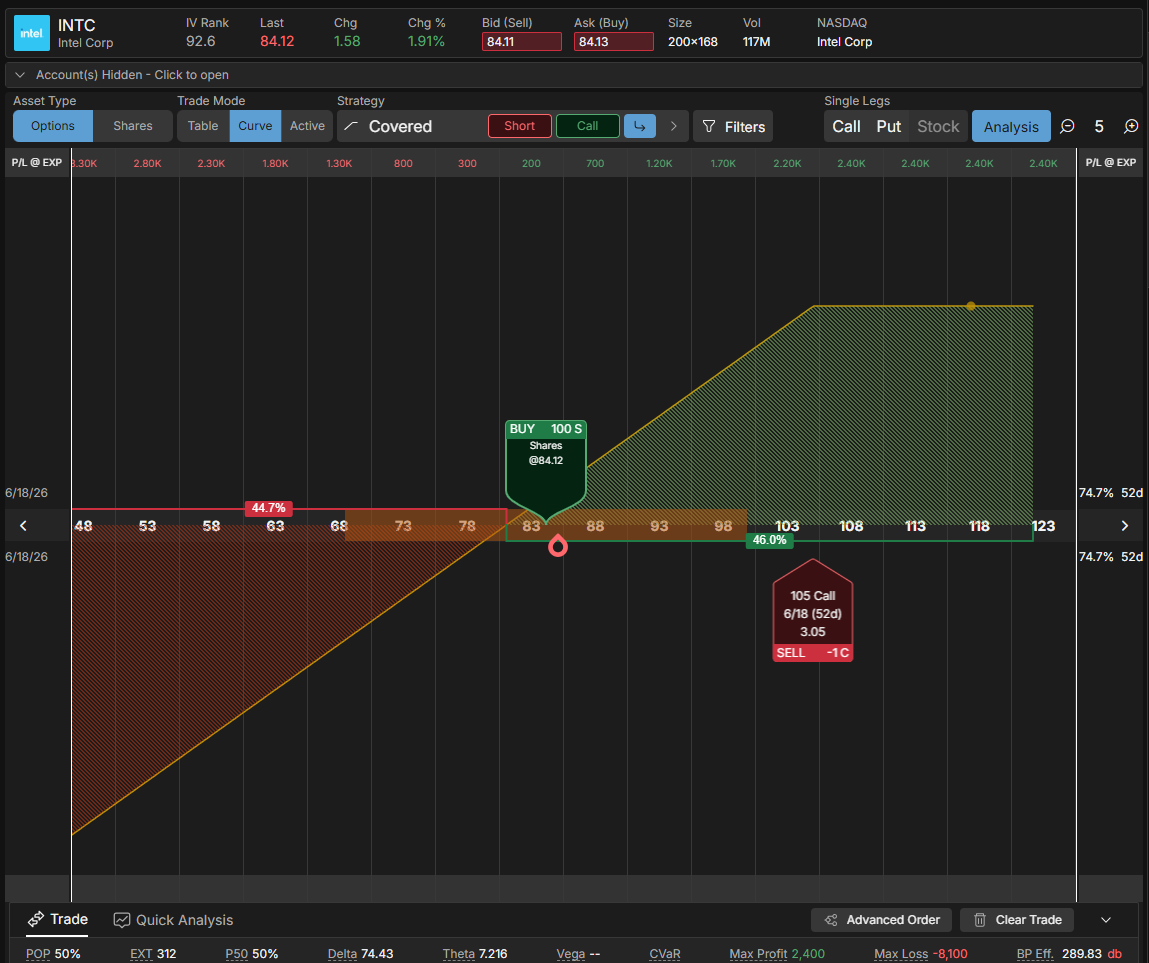

Here is an example of a Covered Call profit and loss graph in INTC. The options table view would be the same as the above image. In the below example, I am buying 100 shares of INTC and selling the $105 Call in the same order. A Covered Call can also be structured with existing shares.

With this trade, we are assuming the price of the stock will stay below our strike and there will be a volatility contraction. We are also betting on Implied Volatility being less than Realized Volatility (which historically it has been). In the above images, I am selling the $105 Call (INTC was trading around $84 when I put this together).

We want to enter this trade when the Implied Volatility (IV) of INTC is high (INTC’s IV Rank was around 93). This way we can benefit from an IV contraction. We also want the price of INTC to stay below $105 through expiration (ideally).

Breaking it Down

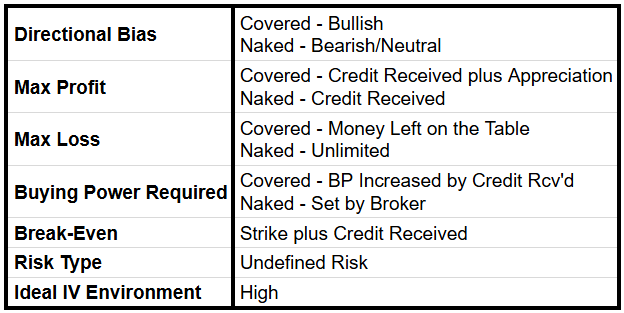

As you may have noticed in my table at the beginning of this post. If we trade Short Calls our bias, max profit, max loss, and Buying Power Requirement depend on if we are Covered or Naked.

When trading as a Covered Call, our bias is Bullish. We truly want the stock to breach our strike. We then walk away with the credit received at entry and appreciation on our shares. If this doesn’t happen, every Covered Call that expires OTM continually reduces our cost basis on our shares. Our max loss is really just money left on the table if the stock soars past our strike. If the stock goes down, that’s a risk we have if we just own the shares anyways. And our Buying Power is actually increased by the credit we received at entry.

When trading a Naked Short Call, our bias is Bearish/Neutral. We make money if the stock moves down, sideways or even up a bit (assuming our strike isn’t breached). Our max loss is unlimited. This is because the stock could move up to infinity. Although it is impossible to lose an infinite amount of money on any trade. Similar to a Naked Short Put, our Buying Power Requirement is based on the broker’s risk analysis. In terms of a max loss, we can use the Buying Power Requirement as a rough estimate. The broker is telling us what their risk is on the trade.

All of that being said, depending on if the Short Call is Covered or Naked, it changes the target credit I aim to collect. If the Short Call is Covered, I aim to receive a premium close to 2% of my cost basis on the shares. For example, if I am selling a Short Call on shares with a $100 basis, I want to receive $2 (100 * 0.02) per share. This target will likely be a little lower with ETFs. If the Short Call is Naked, I aim to receive a credit roughly 20% of the Buying Power held. Usually, I just do a gut check. I look at the credit received and the Buying Power held. If I like the risk/reward, I go in. Although I usually do not open Naked Short Calls on their own.

In this example, if Covered, our max profit is our credit received of $305 plus the appreciation of $2,095 on our shares ((105 - 84.05) * 100). Our max loss is money left on the table or if the stock goes to zero (~$8,100 in the above example [(84.05 - 3.05) * 100]).

If Naked, our max profit is the credit received of $305 (3.05 * 100) and our max loss is ∞ (as stated above).

How do we profit on this trade? We profit if INTC stays below our break-even of $108.05 (105 + 3.05) by expiration, regardless of Covered or Naked. If Naked, ideally, we would like for the stock to stay below our Short strike ($105 in this example). If Covered, it would be most ideal if INTC expires above $105. If the stock price cooperates, we can buy back the Call to close for a debit lower than the credit we received at entry. Or if Covered, we allow for the contract to expire ITM to keep the credit we received at entry and appreciation on the shares. If Naked, we lose if INTC closes above our break-even of $108.05 by expiration. If we are Covered, hold through expiration, AND the price of the stock is above our strike, we will be required to sell our shares. In this example, we would be required to sell shares at a per share price of $105.

There are always tradeoffs with all positions. With a Short Call, we are entering a high Probability of Profit (POP) trade. However, our max profit is capped. We can place our strike at a higher delta. This increases our max profit but reduces our POP. And vice versa with a strike at a lower delta. This trade is more flexible and easier to roll; however, it will price smaller accounts out of certain stocks. And if we have our Short Call Covered, we lock-in a potential price to sell our shares but give up additional upside above the strike ($105 in this example).

With American style options, there is always the risk of early assignment. This is something all traders should be aware of. Especially around ex-dividend dates and earnings. However, if Covered, we are choosing a strike at a price we want to sell our shares anyways. This worst-case scenario is something we want. If Naked and assigned early, we will be required to buy shares at the current market price to close out our Short shares that were assigned. We can also roll out in time well before expiration to mitigate early assignment risk.

Conclusion

Without shares covering the Short Call, I do not like to sell Naked Short Calls on their own. We are fighting against the positive drift inherent in the market. And there are many stocks that it is tough to step in front of the upward momentum. Imagine selling Naked Short Calls in Micron or Sandisk as of late.

The great thing about this strategy (when it is Covered) is it allows us to get paid to (potentially) sell our stock at a price we like. And all contracts that expire OTM or are closed early, effectively lower our basis on the shares. We also profit under several outcomes. This trade profits if the stock moves up, sideways and even up a little. This is the beauty of selling premium.

A Covered Short Call is a great starting point for new traders wanting to dip their toes into “undefined” risk. It has a high POP, can profit in many different market conditions, can be flexible, and we know the worst-case scenario is just selling the shares.

This trade allows for flexibility. Want to increase the max profit? Place the strike at a higher delta. Want to use less Buying Power and you don’t own shares? Place the strike at a lower delta. Want to cover the risk of upside beyond our Short strike? Buy shares at the current market price.

With a Covered Short Call, I do not have a stop loss. It’s okay if a trader does want to utilize one. Personally, I do not see the benefit. Especially since my worst-case scenario is selling the shares (something I want anyways). I will roll an ITM Short Call if it is profitable to do so. A trader may consider utilizing a stop loss when trading a Naked Short Call or covering by buying shares.

I like to sell Short Calls around 30 to 50 Days to Expiration (DTE). A trader can be more aggressive with this though. I know many open these weekly. It’s all very flexible. I look to roll my positions around 21 to 14 DTE. Ideally, if I can roll up a strike AND out in time for a credit, I will do that. I make a decision on whether to close, roll or let it ride at this time.

A common question I see is should I roll my ITM Covered Call? I use an Annualized Return on Investment formula to determine this. That formula is in the image below. If I like the return from rolling, I will do it. If not, I will allow for my shares to be called away.

I recommend closing Naked Short Calls around 50% of max profit. If Covered, we can sit for a little longer, maybe aiming for about 75% of max profit. I usually prefer to take the profits and reenter the trade at a later date. It is not recommended to hold on for more profit. This is because your max profit in the trade remains the same and your risk in the trade has actually increased (max loss AND profit gained). In my opinion, it is not worth it. But it truly comes down to a trader’s own risk tolerance.

Have questions on the Short Call or general feedback for me? Please comment below, I’d love to hear from you!

Question……..last week you listed a few options on your AH poll and POP, but of all the strategies out there which has the highest POP?