The Long Call

Get Upside Exposure to a Stock for a Fraction of the Cost

This week we are going to discuss The Long Call. Many may be familiar with this strategy. This is the last deep dive on these basic legs before I dig into some more intermediate/advanced spreads.

Details

The Long Call is bought with the assumption that the stock will go up in the future. A trader could buy an Out the Money (OTM), At the Money (ATM) or In the Money (ITM) strike. It’s all depending on their risk tolerance and how aggressive they want to be with their assumption.

When buying options premium, it is important to consider what we are agreeing to and what we are actually buying. If the strike is OTM, the trader is ONLY buying extrinsic value. If ITM, the trader is buying intrinsic and extrinsic value. This is important to consider because extrinsic value MUST go to zero by expiration. So, if buying OTM options, a trader is constantly fighting this decay. Due to this, I don’t buy Calls (or Puts) individually very often. I usually use a spread to reduce my cost. Below is an example Long Call profit and loss graph in ETHA 0.00%↑.

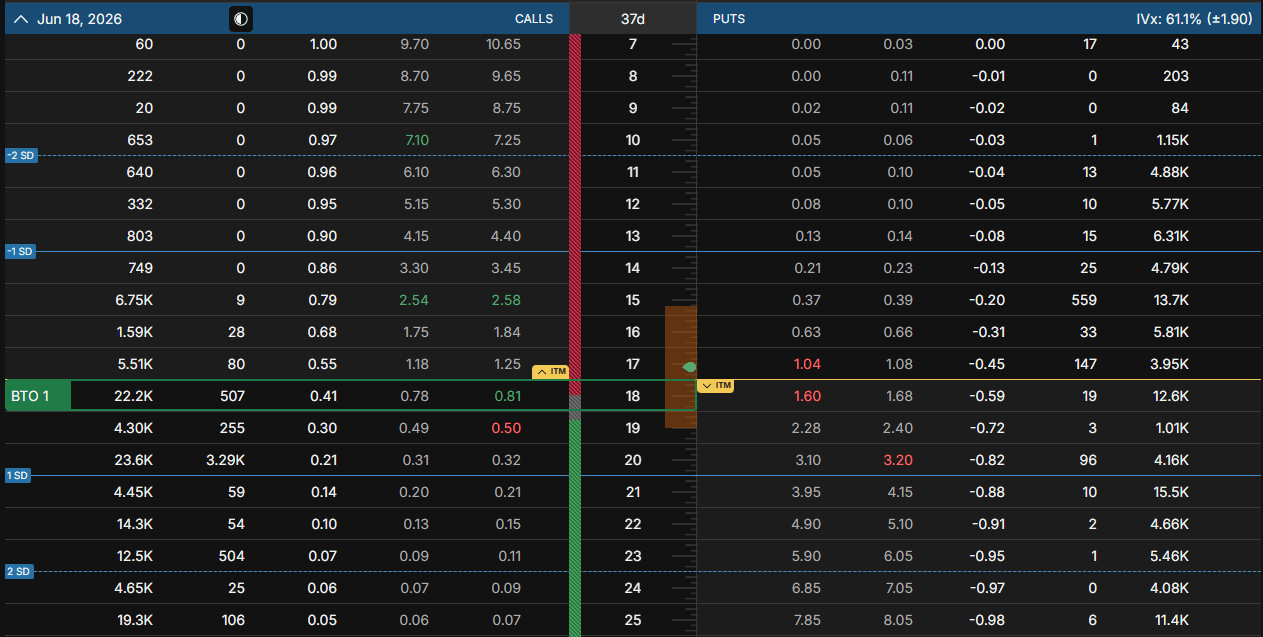

The image below shows how this trade would be structured in an options table.

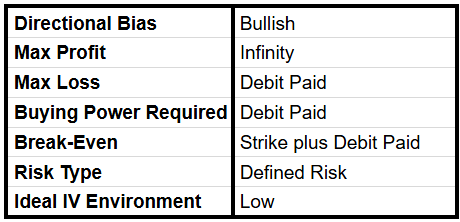

With this trade, we are assuming the price of the stock will go up and there could be a volatility expansion. A Long Call is a defined risk trade; our max loss is the debit paid at entry. In the above images, I am buying the $18 Call (ETHA was trading around $17 when I put this together).

We want to enter this trade when the Implied Volatility (IV) of ETHA is low (ETHA’s IV Rank was around 3). This way we can benefit from an IV expansion (if it happens). We also want the price of ETHA to stay above $18 through expiration (ideally).

Breaking it Down

In order to profit on this trade, we MUST be directionally correct. If the price of ETHA drops, we will lose money. However, all we can lose is the amount we paid to enter the trade.

In this example, our max profit is infinite beyond our break-even price. Although it is theoretically possible, ETHA can’t actually rise to infinity by expiration. Our max loss is our debit paid of $81 (0.81 * 100).

How do we profit on this trade? We profit if ETHA stays above our break-even of $18.81 (18 + 0.81) by expiration. If the stock price cooperates, we can sell to close the Call for a credit greater than the debit we paid at entry. We lose if ETHA closes below our break-even of $18.81 by expiration. Additionally, if held through expiration AND the price of the stock is above our strike, we will be given the option to buy shares. In this example, we could buy shares at a per share price of $18. Buyers have the right to exercise, but they are not required to do so. And buyers can exercise at any point during the duration of the contract with American style options.

There are always tradeoffs with all positions. With a Long Call, we are entering a low Probability of Profit (POP) trade. However, our max profit is theoretically unlimited. We can place our strike at a higher delta. This increases our debit paid and increases our POP. And vice versa with a strike at a lower delta.

Conclusion

The great thing about a defined risk trade is we know our max loss at entry. If sized appropriately, we can sit in the trade. It’s a great way to get upside exposure to 100 shares of a stock at a fraction of the cost. In the above example, I am long 100 shares of ETHA at $18 for only $81 (it would cost $1,710 [17.10 * 100] to buy shares today). However, we profit under only one condition. We MUST have ETHA go up to make money on this Long Call.

When trading all options, it is important to be aware of intrinsic and extrinsic value. If we buy OTM options, we are ONLY buying extrinsic value. We are then constantly battling extrinsic value decay. If we buy ITM options, we have intrinsic value in our favor. This makes it so the extrinsic value decay is less severe.

This trade allows for flexibility. Want to increase the POP on the trade? Place the strike at a higher delta. Want to spend less money at entry? Place the strike at a lower delta. Want to give yourself more time? Buy a further dated expiration. Want to buy some intrinsic value? Consider going ITM with your strike.

With a Long Call, I do not have a stop loss. It’s okay if a trader wants to utilize one. Personally, I do not see the benefit. This is why size at entry is so important. If our debit paid is our stop loss, we can be patient and wait for the move we expected at entry.

Personally, I do not buy many Long Calls on their own. But if I do, I like to buy Long Calls around 30 to 90 Days to Expiration (DTE). A trader can be more aggressive with this though and go shorter term. Or even do a LEAPS (Long-Term Equity Anticipation Securities) Call, which is typically around 365 DTE or more. It’s all very flexible. As with any trade, it is all up to a trader’s own risk tolerance.

Personally, when I buy Calls, I prefer to do them as LEAPS. I like to give myself at least a year to be right. And when I do buy LEAPS, I usually buy around a 70 to 75Δ Strike. This way I am buying lots of time AND intrinsic value. The tradeoff here is that this becomes a more expensive trade.

When to take profits on a Long Call is up to a trader’s own approach. If a trader buys an OTM strike and it goes ITM, it may be time to consider taking profits. We need to be aware of extrinsic value decay. The longer we wait and closer to expiration we get, the quicker the premium decays. Which will lower our probability of profiting on the trade. If I buy a LEAPS Call, I treat that as a stock replacement. I will hold it until 90 DTE or even less.

Have questions on the Long Call or general feedback for me? Please comment below, I’d love to hear from you!

"need some more deets" means I've done a piss poor job of writing about it lol.

What do you need to know?

https://www.traderdaddy.pro/screeners/leaps

That's my selfish reply, lol.

Great article as always!