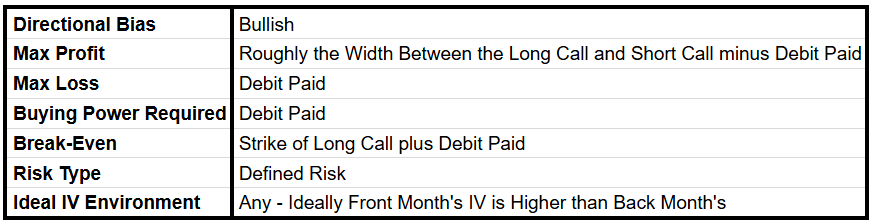

The Call Diagonal

Go Long a Stock While Capitalizing on Short-Term Volatility

This week we are going to discuss The Long Call Diagonal. I like to think of this spread as a type of short-term Poor Man’s Covered Call. We buy a Long Call in a later term expiration and sell a Short Call in a nearer term expiration.

Details

A Long Call Diagonal is bought with the assumption that the stock will go up in the future. The typical construction involves buying a Long Call in a longer dated expiration and selling a Short Call in a shorter dated expiration.

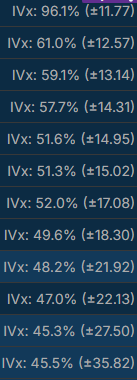

I like Diagonal Spreads as a way to express a bullish (constructed with Calls) or bearish (constructed with Puts) assumption. I will be discussing The Put Diagonal next week, but it is very similar to The Call Diagonal. The great thing about this spread is we use the extrinsic value of the sold Call to offset the cost of the bought Call. This is a great earnings trade since the nearer term Short Call will have a higher Implied Volatility (IV) compared to the IV of the Long Call. You can see what I mean in the image below for NVDA 0.00%↑. The IV Index (IVx) is higher in the near term because earnings are announced after close today.

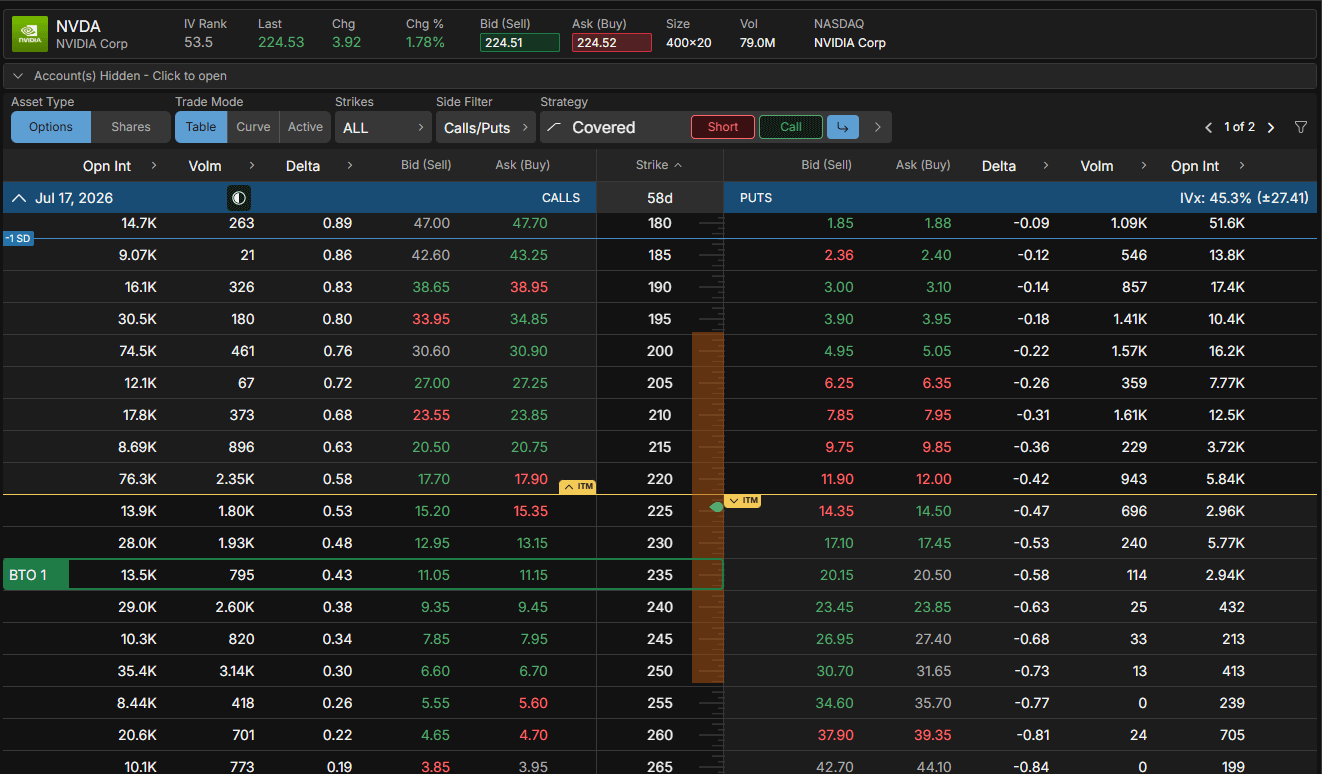

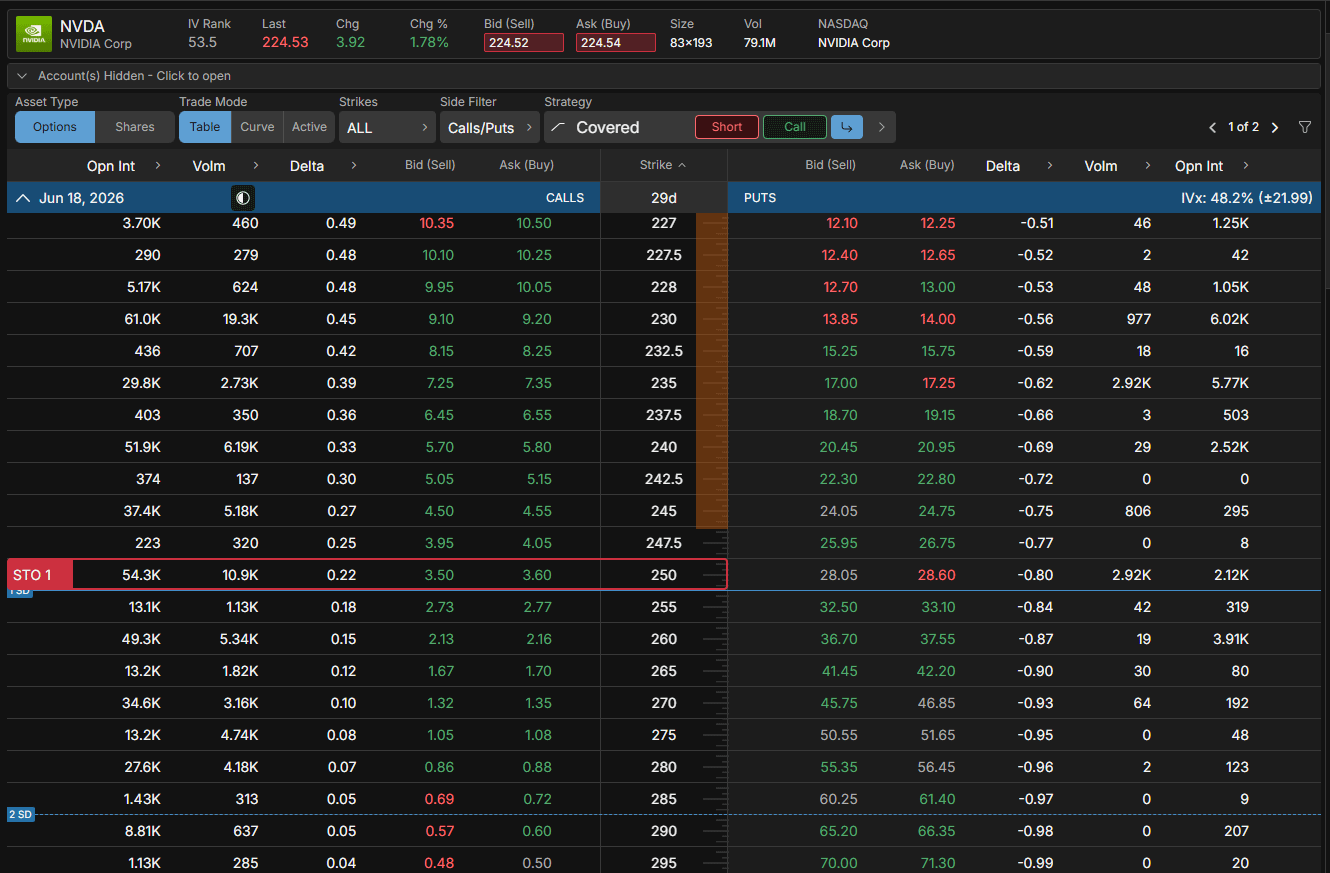

Below is an example Call Diagonal profit and loss graph in NVDA. This is a trade I may enter later today!

The image below shows how this trade would be structured in an options table.

With this trade, we are assuming the price of the stock will go up. A Call Diagonal is a defined risk trade; our max loss is the debit paid at entry. In the above images, I am buying the $235 Call in the July 17th expiration and selling the $250 Call in the June 18th expiration (NVDA was trading around $224.53 when I put this together). This trade would be routed for around a $765 debit ((11.15 - 3.50) * 100).

Ideally, we want to enter this trade when the IV of the stock is higher in the near term. This is why it is a great earnings trade. This way we can benefit from an IV crush in the Short Call. We also want the price of NVDA to stay above $235 through expiration (ideally).

Breaking it Down

In order to profit on this trade, we MUST be directionally correct. If the price of NVDA drops, we will lose money. However, all we can lose is the $765 we paid to enter the trade. Additionally, we give ourselves time to be right by buying that Long Call in a later expiration date.

With a Call Diagonal, our max profit is roughly the width of the spread minus our debit paid. In this above example, our max profit is roughly $735 (((250 - 235) - 7.65) * 100) and our max loss is our debit paid of $765. I say that the max profit is roughly the width of the spread. This is because the extrinsic value of the longer dated Long Call can allow us to profit at a slightly larger amount of the spread width.

How do we profit on this trade? We profit if NVDA stays above our break-even of $242.65 (235 + 7.65) by expiration. If the stock price cooperates, we can sell to close the spread for a credit greater than the debit we paid at entry. We lose if NVDA closes below our break-even of $242.65 by expiration.

When constructing this trade, I like to buy the Long Call that is about a 40 to 50Δ and around 45 to 90 Days to Expiration (DTE). I then like to sell the Short Call that is about a 20 to 25Δ and around 30 DTE or less. Additionally, I like to pay a debit that is roughly one half the width of the spread. In this example, that would be $750 ((250 - 235) * 0.50 * 100). A trader can spend up to 75% of the width of the spread, but it is not recommended to go much higher. It just makes the risk/reward much less attractive.

There are always tradeoffs with all positions. With a Call Diagonal, we are reducing our debit paid by selling that Short Call. But it does reduce our max profit as well. Further, the structure of this trade can be flexible. A trader can experiment with different expirations and deltas. One additional benefit is we give ourselves time to be right here. This way, if the stock begins to drop, we can buy that Short Call back. Which then leaves us with a cheaper Long Call if the stock does rebound.

Conclusion

The great thing about a defined risk trade is we know our max loss at entry. If sized appropriately, we can sit in the trade. A Call Diagonal is a great way to get about 20 deltas of upside exposure for a small debit (40 Long Δ minus 20 Short Δ). However, we profit under only one condition. We MUST have NVDA go up before expiration to make money on a Call Diagonal.

This trade allows for flexibility. Want to decrease the debit paid? Buy the Long Call in a shorter DTE range and at a lower delta. Want to be a little more aggressive? Place the strike of the Long Call at a higher delta. Want to give yourself more time? Buy a further dated expiration. Didn’t get the upside move quickly? Allow for that Short Call to expire worthless or buy it back for cheap. Then sell another Short Call in a new expiration. This will continually decrease the debit paid on the Diagonal.

With a Call Diagonal, I do not have a stop loss. It’s okay if a trader wants to utilize one. Personally, I do not see the benefit. This is why size at entry is so important. My debit paid at entry is my stop loss. This way I can be patient and wait for the upside move I expected when I entered the trade.

When to take profits on a Call Diagonal is up to a trader’s own approach. I usually look to take profits once the stock gets close to or beyond my Short Call strike. We need to be aware of extrinsic value decay for the Long Call. The longer we wait and closer to expiration we get, the quicker the premium decays. Additionally, we don’t want to wait for the stock price to get past the Short Call too much. This is because the profit curve begins to flatten on the trade. Causing us to be stuck with a profit around the width of the spread.

Have questions on The Call Diagonal or general feedback for me? Please comment below, I’d love to hear from you!